Every successful business relies on clear and reliable financial reports, and the Expense Recognition Principle plays a vital role in achieving this. By ensuring that expenses are recorded in the same period as the revenue they support, this principle provides a realistic snapshot of a company’s performance.

It’s not just about following accounting rules; it’s about creating financial statements that are transparent, consistent, and easy to understand. These qualities are critical for making informed decisions, meeting regulatory requirements, and maintaining the trust of stakeholders.

Understanding and applying this principle allows businesses to showcase their actual financial health and operate with confidence.

Let’s unpack how the Expense Recognition Principle is more than an accounting guideline and a strategic tool for better financial management.

What Is the Expense Recognition Principle?

The Expense Recognition Principle is a fundamental accounting concept requiring businesses to record expenses in the same period as the revenues they help generate.

Also known as the Matching Principle, it ensures financial reports provide an accurate depiction of profitability by aligning costs with the income they contribute to.

Imagine this scenario: Your company spends AED 50,000 on an advertising campaign in December, which boosts sales to AED 150,000 in January.

According to the Expense Recognition Principle, you wouldn’t record the advertising expense in December when it was incurred.

Instead, you’d record it in January—when it started generating revenue. This alignment gives a clearer picture of how much profit was truly earned in that period.

Why Does It Matter?

Adhering to the Expense Recognition Principle is essential for:

- Accurate Financial Reporting: Properly matching expenses with revenues ensures that profit and loss statements accurately reflect business performance, offering stakeholders a true picture of profitability.

- Regulatory Compliance: Businesses adhering to GAAP (Generally Accepted Accounting Principles) must follow this principle.

- Better Decision-Making: Accurate financial data allows businesses to plan effectively, allocate resources strategically, and make sound investment decisions.

With a solid understanding of this principle, let’s explore its critical role in accrual accounting.

How the Expense Recognition Principle Helps Accrual Accounting

Accrual accounting relies on the Expense Recognition Principle to provide a comprehensive view of a business’s financial health. Unlike cash accounting, which records expenses only when money changes hands, accrual accounting focuses on when expenses are incurred.

Key Advantages

- Aligns Costs with Revenue: Expenses are matched with the revenue they generate, ensuring financial statements reflect the true performance of the business.

- Improves Cash Flow Management: By showing obligations (like unpaid expenses), businesses can better plan their finances.

- Supports Long-Term Planning: Accrual accounting enables businesses to evaluate profitability over time, making it easier to forecast and strategise.

For example, Alaan simplifies accrual accounting by automating expense matching. Once a transaction occurs, its AI-powered tools categorise expenses, verify receipts, and even sync data with accounting software like QuickBooks or Xero. This automation eliminates manual errors and ensures compliance with accounting standards.

Check out all integrations!

[cta-3]

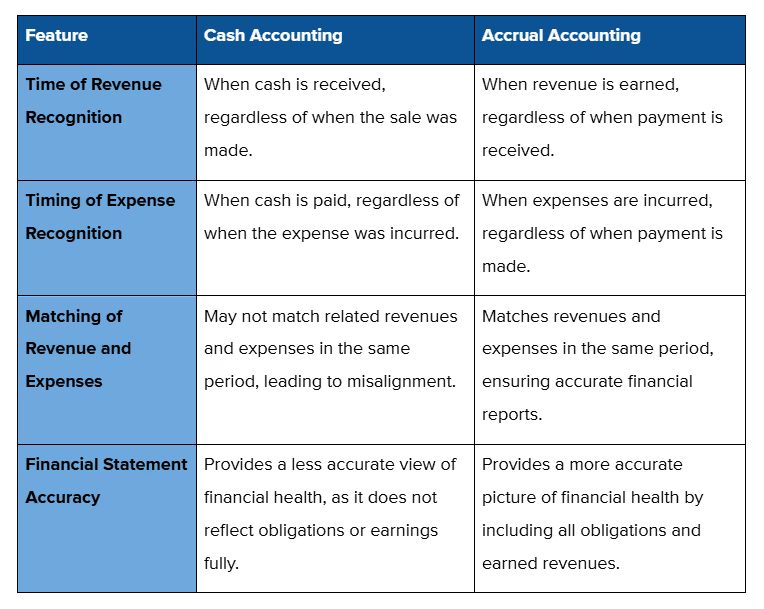

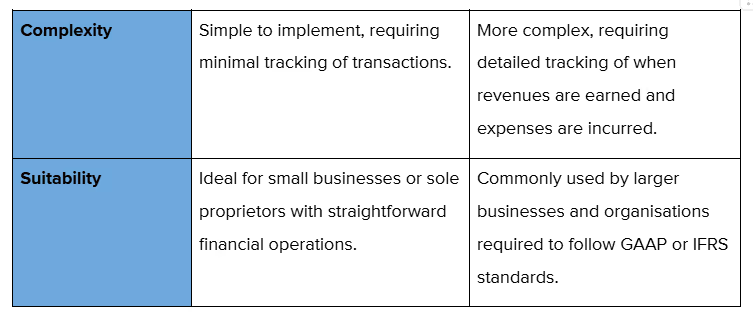

Key Differences: Accrual vs. Cash Accounting

The debate between accrual and cash accounting often boils down to one question: Do you record expenses when they’re incurred or when they’re paid?

Here’s a quick comparison:

An in-depth Look: Difference Between Accrual and Cash Basis Accounting

Why Businesses Choose Accrual Accounting

Accrual accounting gives a more accurate and complete picture of a business’s financial position. For example, a retailer might purchase inventory on credit in November but sell those items in December.

With cash accounting, the expense would be recorded in November, and the revenue would appear in December, creating a mismatch. Accrual accounting, however, ensures both the expense and revenue are recorded in December, giving a clearer picture of profitability.

Make accrual accounting effortless with Alaan. Automatically sync expenses in real time and align them with revenues seamlessly. Book your free demo now!

Now that we’ve covered the differences between these accounting methods, let’s dive deeper into how the Expense Recognition Principle works in practice.

How the Expense Recognition Principle Works

At its core, the Expense Recognition Principle ensures that businesses match their expenses to the revenue they help generate. While this sounds simple in theory, applying the principle can be challenging, especially when dealing with deferred expenses, overlapping project phases, or unpredictable costs.

Yet, the effort is well worth it—it results in financial reports that accurately reflect the performance and health of the business.

When implemented effectively, this principle provides a clear picture of profitability, prevents misalignment between costs and revenue, and supports better decision-making. Let’s break down how it works step by step.

Step-by-Step Process

.avif)

- Identify the Expense

The first step is understanding what costs have been incurred during a specific period. This can include salaries, raw materials, marketing expenses, or even utility bills. Each expense must be carefully recorded to reflect its economic purpose and relevance to the business. For example, if your company hires freelancers for a project completed in December, their fees count as December’s expenses, even if you pay them in January.

- Match the Expense to Revenue

Once you’ve identified an expense, the next step is linking it to the revenue it supports. This is particularly important for businesses that rely on long-term projects or seasonal sales. For instance, if a retail store invests in holiday advertising during November and December, the related costs should be matched with the revenue generated from holiday sales during those months.

- Record in the Same Period

Finally, both the expense and its corresponding revenue must be recorded in the same accounting period. This alignment ensures that your financial statements accurately reflect the cost of generating income, giving stakeholders a clearer picture of your business’s financial health.

[cta-4]

Real-World Examples

To illustrate how the Expense Recognition Principle works, here are a few practical scenarios:

- Labor Costs: Suppose employees complete work in December, but payroll is processed in January. These wages should still be recorded as December expenses since that’s when the work was performed.

- Depreciation: A manufacturing company purchases equipment for AED 100,000 with an expected lifespan of 10 years. Instead of recording the full cost upfront, the business spreads it over 10 years as depreciation, aligning with the revenue the equipment helps generate.

- Marketing Campaigns: A business runs a December campaign that drives sales in January. In this case, the advertising expense should be recorded in January to match the period of revenue impact.

How Alaan Simplifies the Process

With manual accounting, tracking, matching, and recording expenses can be tedious and prone to errors. It eliminates this complexity.

Its AI-powered tools automatically match expenses to revenue, flag discrepancies in receipts, and categorise transactions accurately. This ensures your business adheres to the Expense Recognition Principle without the risk of human error or the burden of manual work.

Understanding how the Expense Recognition Principle works provides clarity on aligning costs with revenues. However, expense recognition doesn’t function in isolation—it operates in tandem with another critical accounting principle: the Revenue Recognition Principle.

Together, these principles ensure that financial statements accurately capture both sides of a business transaction, providing a comprehensive view of profitability.

With that said, let’s look at these hurdles and how to overcome them.

Challenges in Expense Recognition and How to Overcome Them

.avif)

Recognising expenses isn’t always as straightforward as identifying costs and matching them to revenues. In reality, businesses often encounter nuanced and complex scenarios that make the application of the Expense Recognition Principle challenging.

- Complex Transactions

Many businesses deal with transactions that span multiple periods, involve various components, or include intricate cost structures.

For example, a construction company working on a multi-phase project might incur material costs, labor expenses, and subcontractor fees over several months. Breaking down these costs and matching them accurately to their corresponding revenue can be overwhelming without careful planning and robust systems.

The Solution:

Segmentation is critical for managing complex transactions. By breaking down expenses into smaller components and associating each with specific project milestones or revenue streams, businesses can ensure accurate recognition.

Automation tools simplify this process by categorising expenses automatically based on predefined rules.

Its real-time tracking also ensures that costs are recorded as they occur, reducing the risk of misclassification. This streamlining helps businesses manage large projects without compromising on accuracy or compliance.

- Long-Term Obligations

Expenses tied to long-term obligations—such as warranties, service agreements, or leases—require careful allocation over multiple years. For example, if a company offers a five-year warranty on its products, the associated costs must be spread across the warranty period.

Prematurely recognising these expenses can distort profit margins, while delayed recognition can mislead stakeholders about the company’s liabilities.

The Solution:

To handle long-term obligations effectively, businesses should create detailed schedules for amortising these costs. You can automate this process by prorating expenses over their applicable periods, ensuring they’re recognised accurately.

Get a clear view of your future financial obligations with Alaan’s customisable workflows. Track deferred payments and credits effortlessly—schedule your demo today!

- Estimations and Judgments

Certain expenses, such as warranty claims, bad debts, or legal liabilities, often require estimates based on uncertain future events.

These estimations introduce subjectivity and variability, increasing the likelihood of inconsistencies in financial reporting. Moreover, factors like market fluctuations and economic conditions can significantly impact these estimates.

The Solution:

Standardised criteria for making estimations are essential for maintaining consistency. Businesses should document their policies for estimating uncertain expenses, outlining the factors considered and the methodology used.

Regular reviews and adjustments based on updated data can also help ensure accuracy. Alaan supports this process by providing real-time analytics and tracking historical expense patterns, enabling finance teams to make informed judgments with greater confidence.

- Foreign Currency and Exchange Rate Variability

Businesses operating across borders often deal with foreign currency transactions. Fluctuating exchange rates can complicate expense recognition, particularly when there’s a time lag between incurring an obligation and making payment.

For instance, a company might commit to a purchase in euros but pay for it months later when the exchange rate has changed, leading to variances in expense reporting.

The Solution:

Effective currency management is critical in such scenarios. Businesses should monitor exchange rates regularly and use hedging techniques to mitigate risks.

Automation platforms make this easier by supporting multi-currency expense tracking and automatically converting foreign currency transactions into the company’s functional currency. This ensures that any gains or losses due to exchange rate fluctuations are recognised accurately.

- Seasonal Variability

Seasonal businesses, such as retail or tourism, often face misaligned expenses and revenues.

For example, a retailer might incur significant advertising and inventory costs in October to prepare for the holiday shopping season in December. If these expenses are recognised in October, they could misrepresent profitability for that period.

The Solution:

Accrual accounting principles, supported by tools like Alaan, can address this challenge. The customisable workflows allow businesses to allocate expenses dynamically, aligning them with the revenue they generate during peak seasons.

By matching costs to anticipated revenue, businesses can present a clearer picture of their financial performance.

Addressing these challenges requires a proactive and systematic approach. Here are some additional strategies to enhance expense recognition practices:

- Establish Multi-Level Approval Processes: Configurable approval workflows add an extra layer of oversight, preventing errors and misclassifications. For example, Alaan allows businesses to route high-value expenses through multiple approvers before they’re recognised in financial reports.

- Train Finance Teams Regularly: Keeping finance teams updated on accounting standards and best practices is crucial for maintaining compliance. Training sessions that cover complex scenarios, like deferred expenses or multi-currency transactions, can enhance their ability to handle challenges effectively.

By addressing these challenges head-on, businesses can ensure their expense recognition practices are both accurate and compliant. Let’s now discuss when this principle should be applied.

When Should I Use the Expense Recognition Principle?

The Expense Recognition Principle is integral to any business that follows accrual accounting or needs to comply with GAAP. But it’s not just about compliance—it’s about understanding the true costs of generating revenue and making informed decisions.

Common Scenarios for Applying the Principle

- Salaries and Commissions: If employees work in a given month or commissions are earned from sales, these expenses should be recorded in that same month, even if payments are made later.

- Depreciation: Long-term assets, such as machinery or buildings, should be depreciated over their useful life to align the expense with the revenue they generate.

- Inventory Costs: Expenses related to goods sold should be recorded when the goods are sold, not when they are purchased.

How Alaan Helps Businesses Apply This Principle

Using traditional methods to track and allocate expenses can be time-consuming and error-prone.

The real-time integrations with accounting software like QuickBooks and NetSuite ensure that expenses are recorded accurately and consistently. Its customisable workflows also allow businesses to tailor expense recognition practices to their unique needs.

Streamline expense tracking with real-time integrations and customisable workflows!

To further optimise expense recognition, businesses can follow a few best practices.

Best Practices for Expense Recognition

Mastering the Expense Recognition Principle requires more than just understanding it. Businesses need to adopt effective strategies to ensure accuracy and compliance. Here are some best practices:

- Automate Processes

Manual expense management is not only time-consuming but also prone to errors. Misclassified expenses, overlooked receipts, and delayed reporting can all lead to inaccuracies in financial statements. This is where accounting automation steps in as a game-changer.

Helpful Read: Future of Finance Automation in Detail

You can simplify the entire process by automating key tasks such as receipt verification, expense categorisation, and data syncing. For instance:

- When an employee submits a receipt via Alaan’s app, its AI-powered system cross-checks the receipt details (like vendor name, date, and amount) against the corresponding transaction.

- Any mismatches are flagged instantly, ensuring that only accurate data is submitted.

- Once verified, expenses are categorised automatically and synced with accounting tools like QuickBooks or NetSuite.

This level of automation not only reduces the risk of errors but also frees up valuable time for finance teams to focus on higher-value tasks, such as analysing financial trends and supporting strategic decision-making.

Bonus Read: How Corporate Expense Cards Simplify Expense Management

- Ensure Timely Reporting

Timeliness is key when it comes to expense recognition. Delays in submitting, verifying, or categorising expenses can lead to mismatched revenues and expenses in financial statements, distorting the business's true profitability.

To ensure timely reporting:

- Set clear submission deadlines for employees to report their expenses. For example, expenses incurred in a given month should be submitted no later than the first week of the following month.

- Use real-time tracking tools to provide instant visibility into employee spending. They help businesses monitor expenses as they occur, reducing the end-of-month scramble to reconcile and report costs.

- Establish customisable approval workflows to streamline the review process. For instance, a junior sales representative’s expenses might require dual approval from their manager and the finance head, while a senior executive’s expenses might need only one layer of review.

With timely reporting practices in place, businesses can produce accurate financial statements that align expenses with the revenues they support.

- Maintain Transparency

Transparency is the foundation of effective expense management. Without a centralised system for tracking, storing, and managing expense-related documents, businesses risk losing crucial data or failing audits due to incomplete records.

Digitising receipts and invoices is a critical first step toward transparency. Alaan make this process seamless by enabling employees to:

- Upload receipts directly through a mobile app, Chrome extension, or even via email.

- Store digitised versions securely, eliminating the need to maintain bulky paper trails.

- Access and retrieve records effortlessly during audits or internal reviews.

Additionally, the dashboard provides real-time visibility into expense data, allowing both employees and finance teams to track the status of expense submissions, approvals, and categorisation.

This visibility not only builds trust but also ensures that all stakeholders are aligned in their understanding of the company’s financial standing.

- Establish Standardised Policies

Consistency is vital when managing expenses. Businesses should establish clear policies that outline how expenses are classified, approved, and reported. These policies should cover:

- Expense Categorisation: Define categories such as travel, marketing, or office supplies to ensure uniform classification.

- Reimbursement Deadlines: Specify timelines for employees to submit receipts for reimbursement.

- Documentation Requirements: Every expense should have corresponding documentation explaining its purpose, timing, and relation to revenue. The digitised receipt storage simplifies this by creating a centralised repository for all expense records, ensuring transparency and traceability.

Standardised policies minimise discrepancies and provide employees with a clear framework to follow, reducing confusion and improving compliance.

- Use Data Analytics for Continuous Improvement

Expense management isn’t just about recording costs—it’s about optimising them. Businesses should regularly analyse expense data to identify trends, areas of overspending, and opportunities for cost reduction.

With Alaan’s AI-powered insights, businesses can:

- Monitor spending patterns across departments or teams.

- Identify recurring high-value expenses and evaluate their ROI.

- Detects outliers or unusual spending behaviors, such as duplicate expenses or excessive claims in specific categories.

These insights empower finance teams to make data-driven decisions that enhance budget management and improve overall efficiency.

Also Read: The future of AI in Finance: How is AI reshaping the financial landscape?

- Conduct Regular Audits

Audits are essential for ensuring that expense recognition practices align with accounting standards and internal policies.

While annual external audits are standard for most businesses, internal audits conducted quarterly or semi-annually can catch discrepancies early and reinforce compliance.

Digitised record-keeping simplifies the audit process by providing auditors with easy access to detailed expense reports, receipts, and approval workflows.

This reduces the time and effort required to verify financial records and ensures that audits are completed with minimal disruptions to day-to-day operations.

Also Read: How Businesses Can Manage Petty Cash Smartly In 2024

[cta-5]

Conclusion

The Expense Recognition Principle is not merely an accounting rule—it’s a cornerstone for producing accurate, reliable, and transparent financial statements.

By matching expenses with the revenues they help generate, businesses gain a clearer understanding of their profitability, enabling smarter decision-making, establishing stakeholder confidence, and ensuring compliance with regulatory standards.

However, implementing this principle can often be challenging without the right tools. That’s where Alaan steps in.

With features like AI-powered receipt verification, customisable approval workflows, and real-time accounting integrations, it simplifies the complexities of expense recognition.

It empowers businesses to save time, reduce errors, and focus on strategic growth rather than operational bottlenecks.

Ready to take your expense management to the next level? Book a free demo with Alaan today and discover how seamless and efficient financial operations can be with the right solution in place.