Every business expects payment for its products or services, but in reality, not all customers settle their invoices. Some delay payments for months, while others never pay at all, leading to cash flow issues, financial inaccuracies, and unexpected losses.

In the UAE, bad debt is becoming a growing concern, with unpaid invoices now making up 11% of all B2B sales—up from 8% last year. The problem is not limited to large corporations—17% of small and midsize businesses (SMBs) have outstanding debt ranging from $100,000 to $250,000, highlighting the risks of extending credit without proper tracking.

Unpaid invoices may seem minor at first, but they can strain a business financially over time. Without proper tracking, companies may overestimate revenue, struggle with liquidity, or even face tax complications.

That’s why calculating and managing bad debt expenses is essential. In this post, you’ll learn what bad debt expense is, how to calculate it, and the best strategies to track and reduce it—ensuring better financial stability and cash flow.

[cta-3]

What is Bad Debt Expense?

Bad debt expense refers to money a business expects to receive but never does. It happens when customers fail to pay their invoices, leaving the company with an unrecoverable financial loss.

In simple terms, bad debt occurs when a sale is made, but the payment remains outstanding for an extended period—eventually becoming uncollectible. This can happen for several reasons:

- Customer bankruptcy: The customer goes out of business and cannot pay.

- Disputes over goods or services: The customer refuses to pay due to dissatisfaction with the product or service.

- Financial mismanagement: The customer lacks the funds to make payments.

- Fraudulent transactions: Some customers may intentionally avoid payment.

For businesses that offer credit sales, bad debt is an unavoidable reality. While extending credit can boost sales and attract customers, it also comes with risks—especially if your business doesn't have proper tracking systems in place.

To ensure accurate financial reporting, you must record bad debt expenses in your accounting books. This prevents them from overstating revenue, misjudging cash flow, or facing unexpected losses when payments don’t come through.

Why Tracking Bad Debt Expense is Important

Unpaid invoices don’t just affect your revenue—they impact your entire business. If bad debt goes unnoticed, it can distort financial reports, create cash flow shortages, and weaken business stability. Here’s why tracking bad debt is essential:

1. Accurate Financial Reporting

When businesses extend credit, they expect to receive payments. But if a portion of those payments never comes in, failing to account for bad debt can inflate revenue figures and misrepresent the company’s actual financial health.

Recording bad debt expense ensures that financial statements reflect realistic income expectations.

2. Cash Flow and Liquidity Management

Cash flow is the lifeblood of any business. If bad debts accumulate, businesses might run out of available funds for salaries, supplier payments, and operational costs.

By tracking bad debt, businesses can adjust budgets, build reserves, and plan for potential revenue shortfalls before they cause serious financial trouble.

3. Risk Management and Credit Control

Monitoring bad debt helps businesses identify patterns in late or non-paying customers. This allows companies to tighten credit policies, adjust payment terms, or introduce stricter screening processes to minimise risk. For instance, if a particular segment of customers frequently defaults, businesses can revise their credit approval process to reduce future losses.

4. Tax and Compliance Benefits

In some cases, businesses can write off bad debt as a tax-deductible expense, lowering their taxable income. However, to benefit from this, companies must properly track and document unpaid receivables. Failing to do so can lead to tax complications and inaccurate financial records.

5. Improved Forecasting and Business Planning

A well-managed bad debt tracking system allows businesses to forecast future losses more accurately. Companies can use past trends to predict the percentage of sales that may become uncollectible, helping them set realistic financial goals, adjust pricing strategies, and allocate resources wisely.

Tracking bad debt expense is not just about recording losses—it’s about understanding financial risks and proactively managing them.

[cta-4]

How to Calculate Bad Debt Expense

Bad debt expense isn't just a financial loss—it’s a predictable part of doing business that you must account for. By calculating bad debt expense accurately, your business can adjust its financial planning, set aside reserves, and prevent cash flow disruptions.

A bad debts expense calculator simplifies the process by providing quick estimates based on past data and outstanding invoices, ensuring better financial preparedness.

There are two primary methods used to calculate bad debt expense:

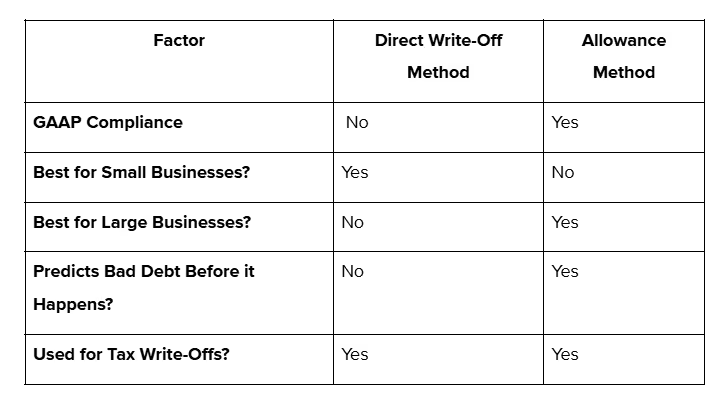

1. Direct Write-Off Method

The direct write-off method records bad debt only when a business confirms that an invoice is uncollectible. This method is straightforward but has limitations, as it does not comply with Generally Accepted Accounting Principles (GAAP) because it fails to match bad debt expenses with the revenue they relate to.

How it works:

- The business attempts to collect an overdue invoice.

- If the customer does not pay after multiple collection attempts, the invoice is written off.

- The business makes a journal entry to debit the bad debt expense account and credit accounts receivable.

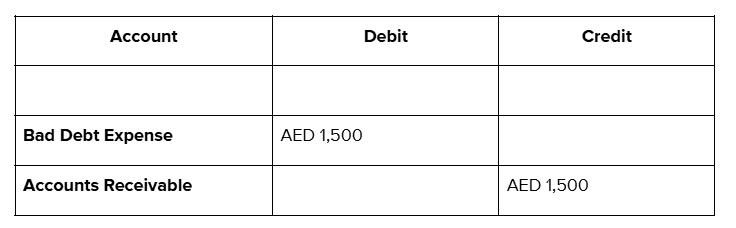

Example journal entry:

Let’s say a business sells AED 1,500 worth of products on credit, but the customer never pays. The journal entry to record this bad debt would be:

When to use: The direct write-off method is suitable for small businesses with low credit sales volume or occasional bad debts. However, larger businesses should use the allowance method for better financial accuracy.

2. Allowance Method (GAAP-Compliant Approach)

The allowance method estimates bad debts before they occur, ensuring a business accounts for uncollectible receivables in the same period the related sales were recorded. This approach aligns with GAAP and accrual accounting principles, providing a more accurate financial picture.

To streamline the process, businesses can use a bad debts expense calculator to estimate the required allowance for doubtful accounts, improving financial planning and accuracy.

How it works:

- The business estimates bad debt based on past data.

- A reserve fund, known as the Allowance for Doubtful Accounts, is set up to offset potential losses.

- When an invoice is deemed uncollectible, the amount is deducted from this reserve.

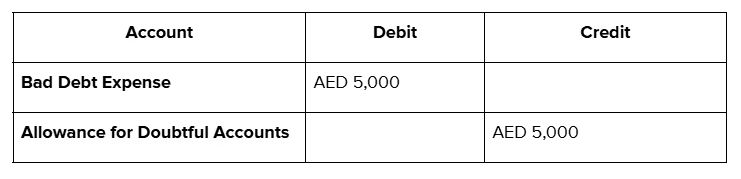

Example journal entry (Creating the Allowance):

If a company expects AED 5,000 of its receivables to go unpaid, the journal entry would be:

When to use: The allowance method is ideal for businesses with frequent credit sales, as it allows them to anticipate losses and maintain financial accuracy.

Methods for Estimating Bad Debt Under the Allowance Method

Once businesses choose the allowance method, they must estimate bad debt expenses using one of the following approaches:

A. Percentage of Sales Approach

This method assumes that a fixed percentage of credit sales will be uncollectible, based on historical data.

Formula: Bad Debt Expense = Percentage of Bad Debt × Total Credit Sales

Example calculation:

A company has AED 500,000 in credit sales for the year and estimates 2% of sales will become bad debt.

Bad Debt Expense = 2% × AED 500,000 = AED 10,000

B. Accounts Receivable Aging Method

This method analyses outstanding invoices by age—the longer an invoice remains unpaid, the higher the likelihood of it becoming bad debt. Businesses assign different percentages of bad debt risk to different aging categories.

Example aging schedule:

When to use: The aging method provides a more precise estimate, making it useful for businesses with large or unpredictable receivables.

Choosing the Right Method for Your Business

Best Practices for Tracking and Managing Bad Debt

Tracking bad debt is more than just an accounting task—it’s a crucial part of maintaining your business’s cash flow and financial stability.

If you fail to monitor overdue invoices, you risk overstating revenue, mismanaging liquidity, and suffering unexpected financial losses. By adopting proactive strategies, you can prevent bad debt from disrupting your finances.

1. Regularly Monitor Your Accounts Receivable

You need to track your accounts receivable closely to identify overdue invoices before they become uncollectible. By maintaining a structured system, you can spot payment delays, assess customer reliability, and take action early.

Using a bad debts expense calculator, you can estimate potential losses and adjust your reserves accordingly, improving financial planning and risk management.

Best practice:

- Review aged accounts receivable reports weekly to track overdue invoices.

- Segment receivables by payment status (e.g., 0-30 days, 31-60 days overdue) to prioritise collection efforts.

- Identify high-risk customers and adjust your credit policies accordingly.

2. Automate Payment Reminders and Follow-Ups

Many unpaid invoices result from delays or forgetfulness rather than intentional non-payment. Automating payment reminders helps you reduce late payments and improve collection rates.

Best practice:

- Send automated email or SMS reminders before the invoice due date and at regular intervals after.

- Implement a structured follow-up schedule:

- 1 day before due date: Friendly reminder.

- 1 week overdue: Second reminder with updated invoice details.

- 2-3 weeks overdue: Phone call or direct email request.

- Beyond 30 days: Escalate to a collections process or legal action.

Using AI-powered automation tools, you can create custom payment workflows based on customer behaviour, making collections more efficient.

3. Define Clear Credit Policies and Screen Your Customers

Offering credit can increase sales, but extending it without a proper evaluation process increases your risk of bad debt. Setting clear credit policies and conducting customer screening can help you avoid payment defaults.

Best practice:

- Perform credit checks on new customers before approving credit sales.

- Set credit limits based on payment history and financial strength.

- Require partial upfront payments for large invoices to reduce risk.

- Establish a clear late payment policy, including penalties for overdue invoices.

4. Use Financial Forecasting to Anticipate Cash Flow Risks

Untracked bad debt can cause unexpected cash shortages. Using financial forecasting tools, like bad debts expense calculator, you can predict how unpaid receivables will impact your cash flow and take action before issues arise.

Best practice:

- Incorporate bad debt projections into cash flow statements.

- Use what-if analysis to model different payment scenarios and their impact on financial stability.

- Adjust budgets and spending plans based on forecasted collections.

By integrating expense management platforms, you can track cash flow in real-time and prevent liquidity issues.

5. Implement a Strong Collection Process

Even with preventive measures, some customers will still default on payments. A structured collection process ensures you recover as much revenue as possible.

Best practice:

- Offer flexible repayment options (e.g., instalments) for struggling customers.

- Engage a third-party collections agency if invoices remain unpaid after 90+ days.

- Document all collection attempts to support potential legal action or tax deductions.

By tracking customer payment history, you can categorise customers by payment reliability and adjust follow-up strategies accordingly.

6. Leverage AI and Automation for Expense and Receivables Management

Manually tracking bad debt is time-consuming and prone to errors. You can significantly reduce financial risk by using automation tools for receivables management.

Best practice:

- Automate invoice tracking, reminders, and overdue follow-ups.

- Use AI-powered analytics to predict which customers are most likely to default.

- Integrate expense and receivables tracking with accounting systems for seamless reporting.

Using an AI-driven platform like Alaan, can help maintain real-time financial visibility, reducing the risk of untracked bad debts.

[cta-5]

How Alaan Helps You Minimise Bad Debt Risks

Managing bad debt starts with financial visibility, automation, and proactive tracking. If you struggle with uncollected payments, it’s likely because you lack real-time oversight of your expenses and receivables.

At Alaan, we simplify financial management by helping you track spending, automate processes, and maintain accurate records—reducing the risk of mismanagement and unexpected losses. Here’s why businesses choose Alaan:

1. Automated Expense Tracking to Prevent Financial Blind Spots

Losing control over finances often happens due to disorganised spending records and manual tracking errors. Alaan ensures that every expense is automatically recorded and categorised, so you can detect potential bad debts before they escalate.

- Instant transaction visibility: Monitor all spending in real-time, preventing untracked or excessive expenses.

- Receipt digitisation: Your employees can instantly upload receipts using the Alaan app or Chrome extension, eliminating missing documentation issues.

- AI-driven expense categorisation: Alaan automatically assigns expenses to the right accounts, reducing errors in financial reporting.

With better expense tracking, you can maintain accurate financial statements, set clear budgets, and prevent cash flow surprises.

2. Seamless Integration with Your ERP and Accounting Systems

One of the biggest challenges in managing bad debt is ensuring accurate financial data flows across different systems. Manual data entry increases the risk of reporting errors and missed receivables.

Alaan integrates with leading accounting platforms like Xero, QuickBooks, Oracle NetSuite, and Microsoft Dynamics, ensuring that all expenses and payments are seamlessly recorded. This allows you to:

- Automate VAT compliance by ensuring all transactions are accurately logged.

- Synchronise expense data in real-time, reducing reconciliation errors.

- Generate up-to-date financial reports, improving decision-making on credit policies.

By eliminating manual processes, you can reduce human errors and maintain accurate financial insights—critical for preventing bad debt.

3. Real-Time Financial Insights for Better Decision-Making

Alaan provides real-time dashboards and analytics that help you spot trends in receivables and identify potential cash flow risks. Instead of waiting until an invoice is overdue, you can take proactive steps to mitigate late payments.

- Predictive analytics highlight which customers are more likely to default based on payment history.

- Customisable reports allow you to track overdue invoices and adjust credit policies accordingly.

- Approval workflows ensure that financial decisions align with your budget and compliance requirements.

With instant access to financial insights, you can make smarter credit decisions and reduce the risk of non-payment.

4. Fraud Prevention and Controlled Business Spending

Bad debt isn’t just about unpaid invoices—it also stems from unauthorised spending, misplaced expenses, and financial mismanagement. Alaan’s AI-powered corporate cards give you greater control over employee spending.

- Customisable spending limits: Set daily, monthly, or merchant-specific limits to prevent excessive spending.

- Real-time transaction tracking: Every purchase is instantly recorded, reducing expense discrepancies.

- AI-powered fraud detection: Identify duplicate transactions, unauthorised purchases, or policy violations before they become financial risks.

By eliminating uncontrolled spending, you can reduce financial leaks, prevent untracked liabilities, and maintain healthier cash flow.

5. AI-Powered VAT Compliance and Reconciliation

For businesses in the UAE, accurate VAT reporting is crucial—especially when managing bad debt write-offs. Alaan ensures seamless VAT compliance by automating tax tracking and reconciliation.

- Auto-extraction of VAT details from invoices to ensure compliance.

- Error detection in financial records, preventing reporting discrepancies.

- One-click reconciliation with ERP systems, reducing manual tax filing efforts.

By automating VAT tracking, you can prevent compliance risks and simplify financial audits.

Conclusion

Bad debt is an inevitable part of doing business, but with the right strategies, it can be managed effectively. Proactive tracking, automated expense management, and smarter credit policies help businesses maintain financial health and prevent revenue losses. By leveraging real-time insights and structured receivables management, companies can reduce risks and improve cash flow stability.

At Alaan, we simplify how businesses track expenses, manage payments, and ensure financial accuracy. Our AI-powered platform automates expense tracking, integrates seamlessly with accounting software, and provides real-time financial insights—helping businesses stay ahead of bad debt risks.

Book a free demo with Alaan today and discover how automation can safeguard your business from financial losses while improving overall efficiency.