.avif)

When it comes to financial reporting, accuracy and consistency aren’t just nice-to-haves—they’re essential. Businesses rely on precise financial data to make informed decisions, but without a universal standard, comparing financial statements across companies becomes confusing and unreliable.

Investors, stakeholders, and regulators must trust that a company’s financials tell a clear, truthful story. Without standardised accounting principles, the risks of errors, misinterpretations, and even fraudulent reporting increase significantly, leaving companies and their investors vulnerable.

This is where GAAP—Generally Accepted Accounting Principles—comes into play. Established to prevent inconsistencies and maintain transparency, GAAP provides a reliable foundation for businesses to present their finances in a clear, comparable, and compliant way.

This blog explores the essentials of GAAP in accounting, covering its 10 core principles, key differences from IFRS, who uses GAAP, and best practices for compliance.

What is GAAP (Generally Accepted Accounting Principles)?

GAAP, or Generally Accepted Accounting Principles, is a standardised set of rules and guidelines for financial reporting.

These principles are created and updated by the Financial Accounting Standards Board (FASB) to ensure all U.S.-based companies, especially public ones, prepare and report their financial information in a consistent and transparent way.

Why is GAAP Important?

Incorporating GAAP principles is essential for maintaining clear, consistent, and trustworthy financial reporting. Here’s why GAAP is so essential in accounting:

- Standardisation and comparability: GAAP makes it easier for investors, regulators, and stakeholders to understand and compare financial statements across different companies.

- Common financial language: It provides a standardised way for companies to report earnings, expenses, and financial health, ensuring consistency across the board.

- Legal requirement for public companies: Publicly traded U.S. companies are legally required to follow GAAP in their financial reports to maintain transparency and compliance.

- Risk reduction: Non-compliance with GAAP can lead to legal consequences, fines, and a loss of investor trust. Following GAAP helps companies avoid these risks.

- Enhanced credibility for private companies: While not required, private companies may choose to follow GAAP to build credibility and attract potential investors.

- Streamlined auditing: GAAP simplifies the auditing process by providing clear standards, enabling auditors to review financial reports more efficiently, thereby saving time and costs.

- Foundation for trust and transparency: Beyond record-keeping, GAAP establishes a reliable foundation for financial transparency, supports informed decision-making, and builds trust among stakeholders.

Now that we know why GAAP is essential, let’s break down the ten core principles that bring these standards to life in financial reporting.

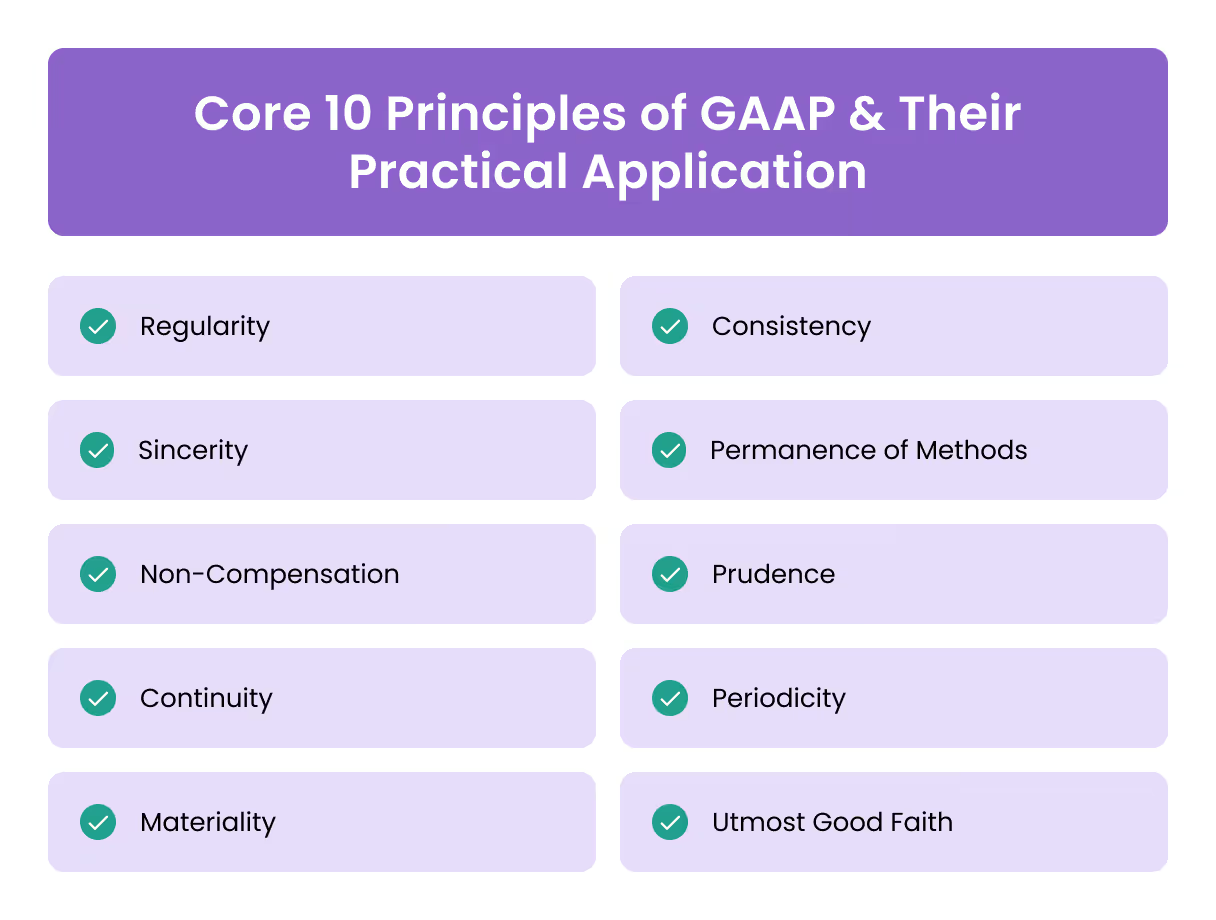

Core 10 Principles of GAAP and Their Practical Application

The foundation of GAAP is built on ten core principles. These principles guide how financial information should be recorded, reported, and interpreted, ensuring that companies present an honest and accurate picture of their financial health.

Here’s a breakdown of each principle and how it applies in practice:

- Regularity

- All financial records should consistently follow GAAP rules.

- Application: A company can’t pick and choose which rules to apply. For example, if a business follows GAAP, it must consistently use the same accounting methods each year.

- Consistency

- Accounting methods should be used consistently across reporting periods.

- Application: If a business starts with one method of recording revenue, it should stick with it unless a clear, documented change is made. This helps to ensure accurate comparison over time.

- Sincerity

- Financial reports should be honest and reflect the true state of the company.

- Application: An accountant must report the actual numbers, even if the business is not performing well, without hiding or inflating financial data to appear more profitable.

- Permanence of Methods

- Companies should use the same accounting methods from one period to the next.

- Application: For example, if a business uses a specific way to calculate depreciation on assets, it should apply that same method each period. This consistency helps investors and analysts make reliable comparisons.

- Non-Compensation

- All financial information, whether positive or negative, should be reported without any offsets.

- Application: Companies must report both gains and losses in full, without using one to cover or “compensate” for the other. For example, revenue can’t be used to hide a debt.

- Prudence

- Financial data should be based on actual facts, not on speculation.

- Application: If there is uncertainty about future profits, accountants should be conservative and avoid recording them until they are confirmed. This principle protects against overestimating assets or earnings.

- Continuity

- Financial reports assume that the business will continue to operate.

- Application: When valuing assets or projecting revenue, it’s assumed the business isn’t closing or being sold. This assumption helps determine asset values more accurately.

- Periodicity

- Financial data should be organised and reported by specific periods (e.g., quarterly or annually).

- Application: A company should report income earned and expenses incurred within the same quarter or year rather than combining or spreading out earnings and costs across periods.

- Materiality

- All significant information that could influence financial decisions must be reported.

- Application: If a company spends a large amount on new equipment, this should be disclosed, as it could impact the financial understanding of the business.

- Utmost Good Faith

- Financial reporting should be conducted with honesty and integrity.

- Application: Accountants are expected to be straightforward in their reports without omitting important details or misrepresenting financial information.

Each of these principles forms a vital part of GAAP, ensuring that financial reports are clear, accurate, and reliable for decision-making.

[cta-10]

Additional GAAP Guidelines: Ensuring Financial Accuracy and Completeness

Beyond the ten core principles, GAAP includes four additional guidelines that ensure financial statements are thorough, clear, and consistently presented alongside the core principles.

Here’s a look at each guideline and how it works in practice:

- Recognition

- All assets, liabilities, income, and expenses must be clearly identified and recorded in financial statements.

- Application: If a company buys new equipment or takes on debt, these should be recognised in its financial reports. Recognition ensures that all relevant financial activities are documented, giving a complete picture of the company’s financial position.

- Measurement

- Financial items should be measured and reported according to GAAP standards.

- Application: GAAP requires reporting assets based on certain valuation methods, like historical cost. This consistency in measurement helps stakeholders compare one company’s financials to another’s accurately.

- Presentation

- Financial statements should include all the essential components: the income statement, balance sheet, cash flow statement, and statement of equity.

- Application: Every financial report should contain these four key sections, each offering specific information about the company’s financial health. Missing any of these could lead to misunderstandings or incomplete analysis.

- Disclosure

- Any extra details or explanations needed to fully understand the financial data should be clearly disclosed.

- Application: If a company has unusual transactions or changes in accounting methods, these should be explained in the report notes. This transparency allows investors and analysts to understand the full context behind the numbers.

Now that we’ve covered GAAP’s foundational principles and guidelines, let’s look at how GAAP compares with another major accounting standard: IFRS (International Financial Reporting Standards).

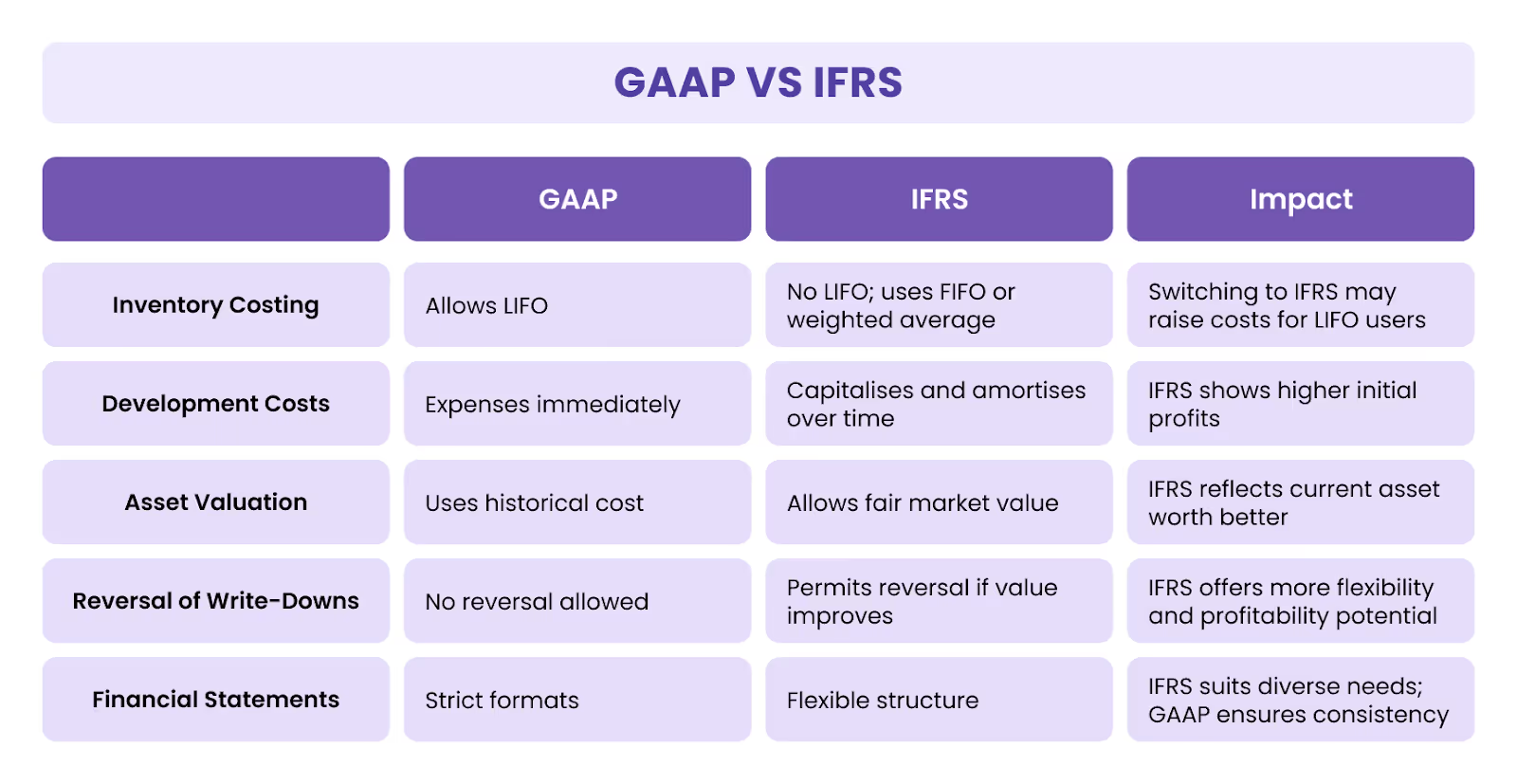

GAAP vs. IFRS: What are the Differences?

GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) are two major accounting standards used globally, but they differ in several key ways.

While GAAP is mainly used in the United States, IFRS is used by over 100 countries, including those in the European Union, Canada, and Australia. Both standards aim to promote transparent and reliable financial reporting, but they have distinct approaches in certain areas.

Here’s a breakdown of some of the main differences between GAAP and IFRS:

- Inventory Costing Methods

- GAAP: Allows companies to use the Last-In, First-Out (LIFO) method, where the most recently acquired inventory is the first to be sold.

- IFRS: Does not allow the LIFO method; companies must use other methods, like First-In, First-Out (FIFO) or weighted average cost.

- Impact: For U.S.-based companies that rely on LIFO for inventory cost savings, switching to IFRS could increase reported costs.

- Development Costs

- GAAP: Typically treats development costs, like research expenses, as immediate expenses when they occur.

- IFRS: Allows companies to capitalise on certain development costs, treating them as long-term assets that are amortised over time.

- Impact: Under IFRS, companies that capitalise on development costs may show higher initial profits, as the expenses are spread out over time.

- Asset Valuation

- GAAP: Requires assets to be valued at historical cost, meaning the original purchase price without adjusting for current market value.

- IFRS: Allows assets to be adjusted to their fair market value, reflecting current prices or conditions.

- Impact: IFRS can lead to higher asset values on the balance sheet, providing a more current view of an asset’s worth.

- Reversal of Write-Downs

- GAAP: Does not allow companies to reverse write-downs on inventory or assets once they have been recorded as a loss.

- IFRS: Permits companies to reverse write-downs if the market value of an inventory or asset improves after a decline.

- Impact: IFRS offers more flexibility for companies to adjust asset values if conditions improve, which could positively impact profitability.

- Presentation of Financial Statements

- GAAP: Provides specific formats and guidelines for organising financial statements.

- IFRS: Offers more flexibility in how financial statements are structured, allowing companies to adjust based on their needs.

- Impact: IFRS may be seen as less rigid, which can benefit companies with unique reporting needs, while GAAP’s stricter guidelines provide consistency across U.S.-based reports.

While both GAAP and IFRS serve the purpose of promoting transparency and consistency, each has its unique advantages and limitations. For companies operating internationally, understanding these differences is essential, as they may need to comply with both standards.

GAAP Compliance: Best Practices and Common Challenges

Ensuring GAAP compliance is essential for businesses that want to maintain accuracy, build trust, and avoid legal issues in financial reporting.

However, keeping up with all GAAP requirements can be challenging, especially as standards evolve. Here are some best practices to help with GAAP compliance and common challenges companies often face:

Best Practices for GAAP Compliance

- Document all financial activities: Keep thorough records of all transactions, including income, expenses, and asset purchases. Proper documentation supports accurate reporting and makes it easier to trace financial data.

- Use consistent accounting methods: Stick to the same accounting practices year after year. If a change is necessary, document it carefully and explain it in financial statements to ensure clarity.

- Invest in accounting software: Reliable accounting software can help automate processes, reduce errors, and keep records in line with GAAP standards. Look for software that offers GAAP compliance features.

- Train staff on GAAP standards: Ensure that your accounting team is well-versed in GAAP principles. Regular training helps staff stay updated on any new or revised GAAP guidelines.

- Conduct regular internal audits: Periodic audits can help catch errors early, ensure compliance, and prepare the company for any external audits. Audits are also a good way to identify any areas needing improvement.

- Establish a clear review process: Before finalising financial statements, review them carefully for accuracy and compliance. Involve multiple team members in the review process to minimise the risk of oversight.

Common Challenges in GAAP Compliance

- Keeping up with changing standards: GAAP is updated regularly to keep pace with financial changes. This can make it difficult for companies to stay current on all requirements.

Our Solution: At Alaan, we simplify compliance by offering real-time expense tracking, seamless accounting integrations, and automated reporting.

Our platform offers businesses instant visibility and control over expenses, from corporate cards to automated invoice payments, ensuring your financial records stay accurate and up-to-date with every change in regulation. Alaan empowers finance teams across industries like Real Estate, Aviation, and Retail, saving both time and money while keeping compliance simple.

- Ensuring consistency across reports: Consistency is a core GAAP principle, but maintaining the same methods over time can be challenging, especially in complex organisations.

Our Solution: Alaan’s customisable spend controls and one-click reconciliation allow you to standardise reporting practices across departments, ensuring consistency.

Our platform ensures that expense data is consistently categorised, tracked, and reconciled, helping finance teams uphold GAAP standards while reducing manual errors.

- Managing disclosures: GAAP requires detailed disclosures for full transparency, which can be time-consuming. Disclosures must be precise and easy for stakeholders to understand.

Our Solution: At Alaan, we streamline this process by providing businesses with accurate, actionable analytics and automated reporting. Our seamless integration with top accounting solutions like Xero, QuickBooks, and NetSuite enables consistent data capture and reconciliation, ensuring all financial records are accurate and disclosure-ready.

By following best practices and using Alaan to tackle common challenges, businesses can simplify GAAP compliance, making financial reporting more reliable and less stressful.

Now, let’s look into the historical context of GAAP and how it has evolved into the essential standard it is today.

[cta-9]

Conclusion

GAAP, or Generally Accepted Accounting Principles, is essential for maintaining transparency, consistency, and trust in financial reporting.

By following GAAP, businesses ensure that their financial statements are accurate, comparable, and aligned with standard practices.

At Alaan, we understand the importance of accurate financial reporting and streamlined expense management. Our AI-powered platform simplifies expense tracking, automates bookkeeping, and integrates seamlessly with your accounting processes to help your business stay compliant with ease.

With 91% of professionals reporting that technology improves productivity and allows them to focus on clients, it’s time to simplify your financial management with Alaan. Save time, reduce manual work, and maintain precise financial records.

If you're looking for a simpler way to manage expenses and stay compliant, Book a free demo today to explore how our platform can save you time, ease the workload, and keep your business running smoothly.